As the National Assembly prepares to dive into intensive legislative debates, the newly unveiled Finance Bill, 2026 has landed on the desks of policymakers and taxpayers alike, signaling a monumental shift in how the state intends to fund its agenda.

At a time when household budgets remain sensitive to inflation and the political stakes are higher than ever, the National Treasury is walking a delicate tightrope. The target is steep: the government is chasing an astronomical revenue target of KSh 3.533 trillion—composed of KSh 2.901 trillion in ordinary revenue and KSh 632 billion in appropriations-in-aid.

However, unlike previous fiscal cycles characterized by aggressive, broad-based consumer tax hikes, the 2026 strategies rely on a more sophisticated mechanism: aggressive tax-base broadening, plugging judicial loopholes, and dramatically tightening compliance windows. National Treasury Cabinet CS John Mbadi has already come out to defend the proposals, urging the public not to misinterpret the provisions, while lawmakers like Embakasi North MP James Gakuya warn that public participation must not be rushed if Kenyans’ voices are truly to be heard.

For corporate Kenya, tech enthusiasts, landlords, and the everyday citizen, here is the comprehensive breakdown of what the Finance Bill, 2026 actually means for your pocket.

1. The Fintech and Banking Squeeze: Overhauling Card Payments & Royalties

Following a series of high-profile legal standoffs between the Kenya Revenue Authority (KRA) and financial institutions, the state has used the Finance Bill, 2026 to systematically rewrite definitions to favor revenue collection.

- The Card Payment Loophole Closes: In an amendment to Section 2 of the Income Tax Act, the Bill expands the definition of “management or professional fees” to explicitly include interchange fees and merchant service fees arising from card-based payment transactions. This effectively subjects these transactional fees to withholding tax, directly countering a major 2025 Supreme Court ruling where banks had successfully argued against such taxation.

- Redefining ‘Royalties’ for the Digital Era: The definition of what constitutes a royalty has been entirely overhauled to loop in modern digital infrastructure. Under the proposed text, a royalty now covers payments for the use of or access to a proprietary digital platform, payment network, payment-card scheme, payment processing system, switching system, clearing system, or settlement system. Crucially, it captures these payments whether they are periodic or transaction-based, regardless of whether they are labelled as network fees, service fees, or processing charges.

- The VAT Digital Strike: Parallel to these definitions, digital and platform-based financial services—including payment gateways and electronic transfers—are slated to face standard-rate VAT, potentially escalating the transactional costs of digital commerce in Kenya.

2. Property and Wealth: Target on Rental Income and Trusts

The real estate sector and wealth management structures are facing structural tax realignments that will trigger mixed reactions:

- The Non-Resident Landlord Net: The Bill introduces an entirely new tax regime under Section 6B known as the Non-Resident Rental Income Tax. Non-resident individuals or corporate bodies deriving income from the use or occupation of Kenyan property will be required to register and account for this tax through a simplified registration framework prescribed by the KRA Commissioner. Returns and payments under this regime will be strictly due on or before the 20th day of the following month, unless the rent is received by a resident agent who undergoes standard withholding processes.

- The Resident Landlord Hike: For local resident property owners, the monthly residential rental income tax rate is set to climb from 7.5% to 10% in a bid to expand the domestic tax yield.

- Streamlining Trusts: To minimize aggressive tax planning, the Bill provides that income received in the capacity of a trustee, executor, or administrator will be legally deemed the income of that trustee. To prevent double taxation, any dividend or interest included in this trust income will not face further taxation, and once the trustee settles the tax, beneficiaries are entirely exempt from liability on that specific income.

3. Compliance Speedrun: Shorter Filing Windows

The KRA wants its money faster, and the Finance Bill, 2026 achieves this by dramatically shrinking traditional tax administration timelines:

- The 4-Month Filing Crunch: In a shocking twist for accountants and taxpayers, the window to file annual income tax returns has been cut down from six months to four months following the end of the year of income. This shifts the traditional June 30 deadline to April 30.

- Nil Returns Tightened: Taxpayers filing “Nil” returns face an even faster turnaround, with the Bill mandating that Nil returns must be submitted within one month after the close of the income year.

- The Calendar Day Trap: Tax compliance experts are raising red flags over a proposed shift in how tax dispute timelines are calculated. The Bill seeks to amend the Tax Procedures Act so that objection and appeal windows are computed on a strict calendar-day basis rather than working days, significantly shortening the preparation time for aggrieved taxpayers.

4. Green Energy Shock, Mitumba Taxes, and Gambling Overhauls

Several key sectors will experience immediate pricing and structural shifts if the Bill passes in its current form:

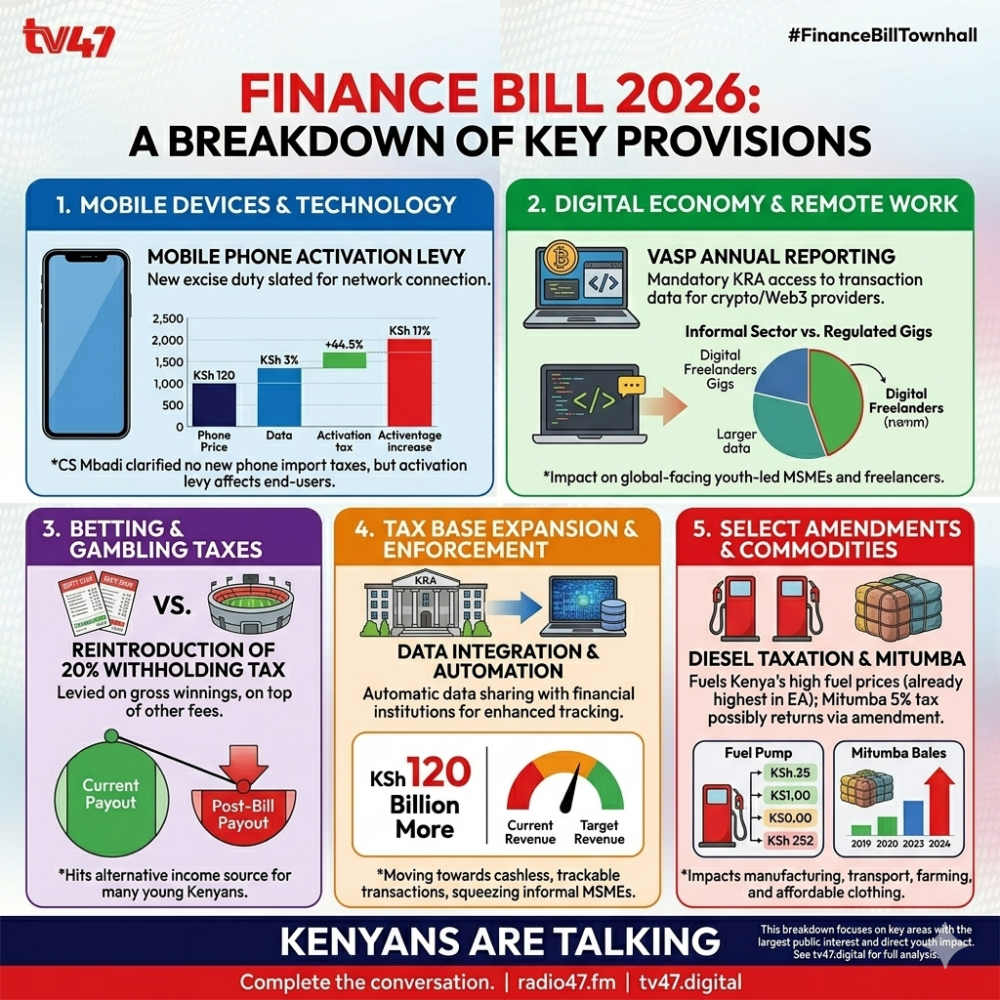

- The E-Mobility and Solar Reversal: In a surprising shift from previous environmental incentives, the Bill introduces a standard 16% VAT on electric motorcycles, electric buses, electric bicycles, solar products, and lithium-ion batteries—a move that could slow down the adoption of clean energy and e-mobility solutions across the country.

- The ‘Mitumba’ Duty: A 5% implied tax on the customs value of imported second-hand clothing and footwear has been proposed to boost local textile industries. Treasury CS John Mbadi clarified that this proposal originally emanated from sector players looking for a simplified valuation process.

- A Deeper Cut into Gambling: The gambling industry faces an expanded tax base. The Bill replaces the previous definition of taxable “withdrawals” to encompass any money, cash equivalent, or money’s worth paid or disbursed directly into a player’s account by a gaming operator. It also formally reintroduces the definition of “winnings” as any payout from a lottery or prize competition, explicitly excluding the initial stake or wager. Winnings and scrap metal sales are both added to the list of items tracking withholding tax.

5. The Silver Linings: Reliefs, Amnesties, and Salary Cushioning

To ensure the Bill remains palatable during public participation, the National Treasury has integrated notable relief windows:

- The USD 2,000 Baggage Relief: In a major victory for international travelers and small-scale traders, the duty-free threshold for accompanied personal baggage at border entry points has been dramatically raised from USD 300 to a generous USD 2,000.

- Tax Amnesty Extension: The widely popular tax amnesty on penalties, interest, and fines has been extended to December 31, 2025, provided that the underlying principal tax liability is fully settled on or before December 31, 2026.

- Instalment Tax Relief for Employees: Taxpayers whose sole source of income consists of employment emoluments are officially exempted from the tedious requirement of paying instalment tax.

- CBK Housing Perks: For workers utilizing housing programs, the Bill allows an income tax deduction of up to KSh 360,000 on interest paid toward home construction or purchase loans advanced directly by the Central Bank of Kenya.

- Gratuity Protections: For those on contract terms, the Bill expands tax-exempt considerations on gratuity contributions, provided the contract of service spans a continuous period of at least three years and total contributions do not exceed 31% of the employee’s basic salary.

The Bottom Line: A “Silent Squeeze”

The Finance Bill, 2026 represents a masterclass in fiscal subtlety. By steering clear of highly visible consumer price shocks on everyday household staples, the government hopes to maintain political stability and avoid public unrest.

However, corporate and tech-dependent Kenyans should make no mistake: the “silent squeeze” is highly real. By targeting the digital ecosystem, shortening compliance windows to four months, and bringing transaction-based card processing platforms under the withholding tax net, the KRA has designed a net that is wider, tighter, and faster than ever before.

Follow our social media pages for a live coverage of the Finance Bill Townhall coversation with CS Mbadi today from 6.00 pm.

For real-time updates and breaking news alerts on the Finance Bill 2026 legislative debates, SMS ‘NEWS’ to 20374.